By March 20, the price of Russian pig iron on an FOB Black Sea basis had risen to USD 340/t, after falling from USD 335/t to USD 325/t between February 17 and March 3. Meanwhile, domestic prices remain steady at around RUB 25,550/t.

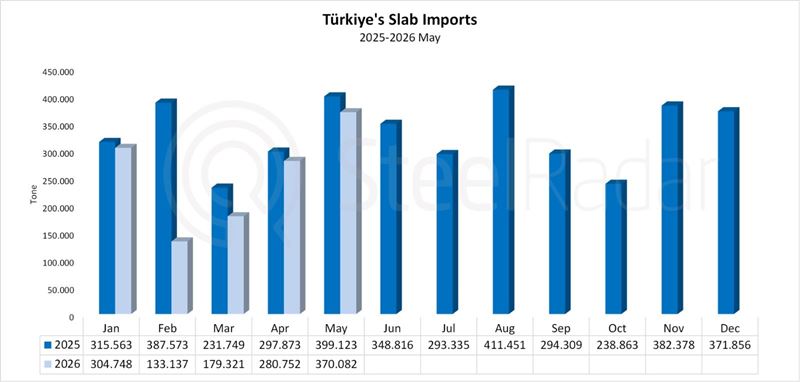

The rebound in prices is largely driven by stronger demand for scrap in Türkiye, where imported scrap was trading at approximately USD 380/t (CFR) at the end of last week, with Russian-origin scrap at USD 340–350/t.

With EU quotas for Russian pig iron fully used up, Türkiye has emerged as the key market for Russian exporters. Other buyers in Asia, including India, continue to offer prices below USD 300/t FOB Black Sea, making those destinations less attractive. Only a few Russian producers have adjusted their production in response to changing market conditions. For example, Severstal reduced its pig iron output by 11% year-on-year in 2024 to 10 million tonnes, while MMK scaled back production by 4.5% to 9.5 million tonnes.

The EU's import quota for Russian pig iron stood at 1.14 million tonnes in 2024 and was exhausted by September. For 2025, the quota was slashed to 700,000 tonnes, which was fully used up by mid-March. Starting in 2026, the EU plans to phase out Russian pig iron imports entirely.

In January 2024, global pig iron production saw a marginal year-on-year increase of 0.1%, but dropped by 2.2% compared to December. Meanwhile, the EU expanded its trade surplus in pig iron and steel to €4.7 billion, driven by increased export value and higher import value compared to 2019, despite lower physical volumes. Key EU trade partners in these sectors included Türkiye, the United States, and the United Kingdom.

Some volumes of Russian pig iron delivered to the EU after the 2024 quota was exhausted were stored in European ports until the new quota period began. Due to the significantly reduced 2025 quota, allowed volumes were quickly depleted in the first quarter. Despite the restrictions, Russian pig iron remains in demand in the EU thanks to its discounted pricing, with main buyers being Italy, Latvia, and Poland. However, no signs have emerged suggesting the EU will reverse its decision to ban imports from Russia.

The increased focus on Türkiye as an export destination is seen as a forced move. Since October 2024, Türkiye has imposed duties of 6.1–9% on imported flat steel from Russia, adding to challenges already exacerbated by the weakening Turkish lira. Under these conditions, securing new alternative markets is proving difficult for Russian exporters.

There is some potential to redirect volumes to countries like the UAE, Egypt, and parts of Africa. These markets may purchase pig iron for local steel production or re-export it through third-party traders to destinations such as the EU. However, even in these relatively neutral regions, competing with Chinese suppliers remains a significant challenge.

A possible reduction in Chinese steel production by 50 million tonnes in 2025 could provide short-term support for raw material prices, as expectations of higher steel prices grow. Nonetheless, excess global steelmaking capacity will continue to weigh heavily on the market in the long term.

Comments

No comment yet.