Russian billet export prices have declined further amid weak demand from Türkiye and North Africa, as well as lower price expectations from buyers. Current offers for November–December shipment are reported at $440–442/t FOB Black Sea.

A recent deal confirmed the market’s downward movement: Metalloinvest sold 50,000 t of billet to Habas at $445–447/t CFR Türkiye, while other offers are heard at $450–460/t CFR Türkiye and $430–435/t FOB Black Sea.

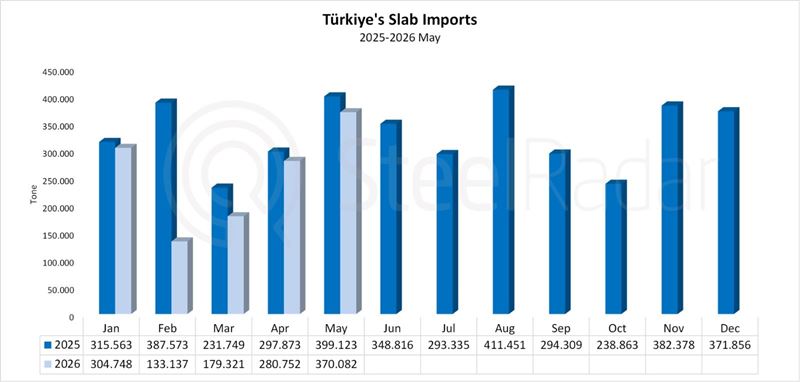

Market participants attribute the latest decline to weak demand and new Turkish import restrictions, which took effect on October 1. Under the new rules, Turkish processors must source at least 25% of their semi-finished or finished steel from domestic producers, limiting import opportunities.

Demand from North Africa remains subdued, with Egyptian billet buyers adopting a wait-and-see approach. Freight rates for smaller cargoes reflect the cautious trading sentiment: shipping 5,000–6,000 t of billet from Reni/Izmail to North Africa costs around $36/t, while delivery to Marmara is priced at about $23/t.

According to Viktor Tarnavsky, Head of Analytics at Metallosnabzhenie i Sbyt, Russian mills reduced prices for November contracts as Chinese billet became cheaper, further increasing competition. He added that while Russian steel exports have risen in recent months, they still account for no more than 10% of total production.

This year, Russian metallurgists are benefiting from exports not as a major source of profit—given the ruble and dollar exchange rates, the profitability of foreign sales remains limited—but as a way to maintain capacity utilization and avoid plant closures or mass layoffs. However, analysts note that financial risks in the real sector are gradually increasing.

On the global stage, the steel market remains quiet. China continues to increase exports, unable to offset declining domestic demand that has persisted since 2021. At the same time, more countries are introducing barriers to steel imports. When large importers such as the US, EU, India, Brazil, and Türkiye restrict steel inflows, competition in the remaining open markets intensifies. The past few months have also seen a rise in anti-dumping cases against steel suppliers, particularly targeting hot-rolled and stainless steel products.

Slight price gains in Iranian and Thai billet markets suggest a slow recovery in regional demand across Asia and the Middle East. Meanwhile, stable scrap and coal prices indicate a balanced raw material chain.

Market participants expect Russian billet prices to remain under pressure through the coming weeks unless a significant improvement in Turkish or North African demand materializes.

Comments

No comment yet.