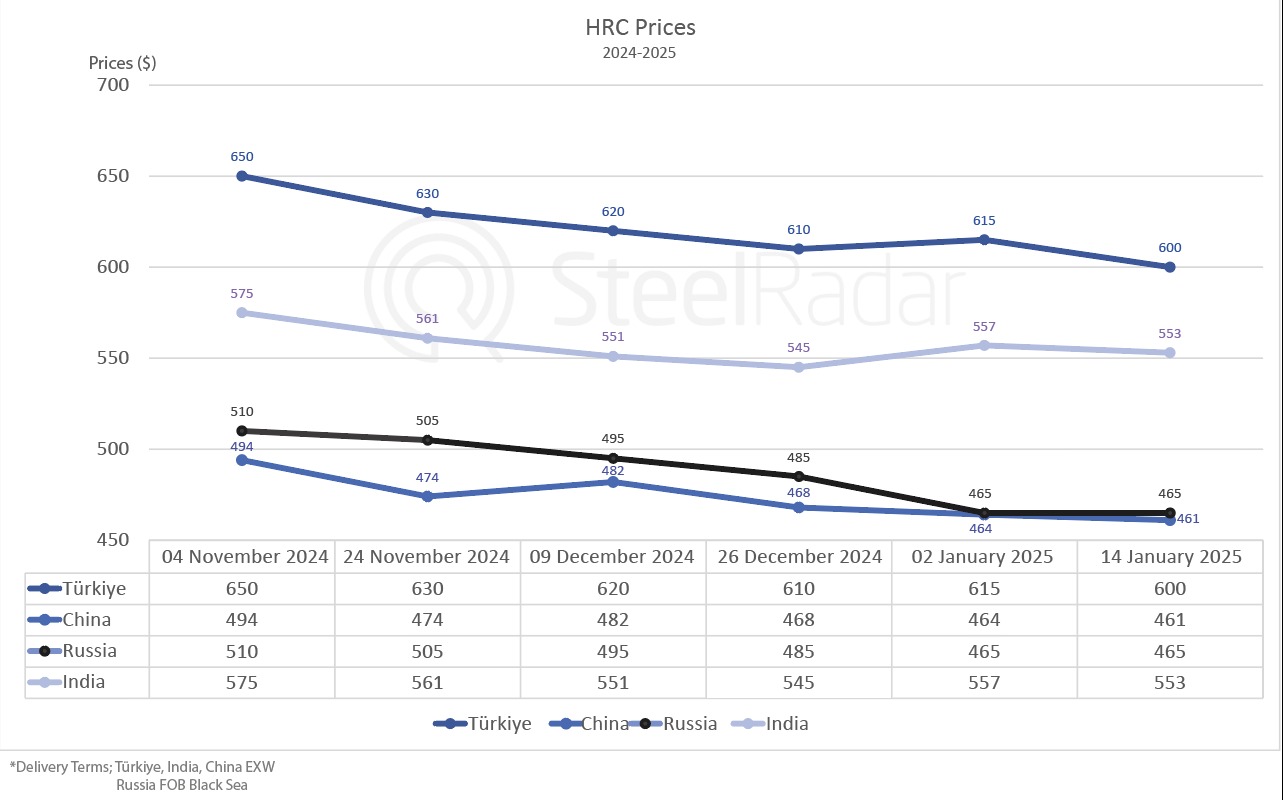

The Global HRC Market

HRC prices have continued to weaken across major markets. In the Persian Gulf (GCC), Chinese HRC offers fell by $10–$15 per ton in early January 2025, reaching $500–$505 per ton CIF. Indian mills reduced their offers to $535 per ton CIF but encountered resistance from buyers unwilling to go beyond $525 per ton for February shipments. Market analysts expect these lower price levels to become the norm by February, reflecting ongoing pressures on suppliers.

Russian-origin HRC prices followed a similar downward trajectory. Offers started the year at $580 per ton FOB Baltic Sea and $590–$595 per ton FOB Black Sea but tumbled to $490 per ton FOB Black Sea by the end of 2024. Transactions in key markets such as Türkiye and Egypt also declined, highlighting reduced demand and fierce competition from low-priced Asian suppliers.

The global oversupply of HRC is partly attributed to Russia’s suspension of export duties, which has exacerbated competition. Asian manufacturers, particularly from China, have flooded the market with aggressively priced steel, intensifying pressure on producers. Meanwhile, economic slowdowns in Europe and Türkiye, along with reduced activity in steel-consuming industries, have further dampened demand.

Ship Prices Rise Facing Regulatory and Geopolitical Pressures

In stark contrast to the HRC market, ship prices have been on an upward trajectory. This paradox can be attributed to a confluence of regulatory, structural, and geopolitical factors that have created sustained demand for new and compliant vessels.

The maritime industry faces significant challenges in meeting decarbonization targets set by the International Maritime Organisation (IMO). The IMO has mandated a 40% reduction in carbon intensity by 2030, alongside a requirement for at least 5% of fuels used in shipping to be low-carbon by then.

To comply with these regulations, shipping companies are investing heavily in new vessels powered by clean fuels such as liquefied natural gas (LNG), methanol, or liquefied petroleum gas (LPG). They are also adopting measures like retrofitting older vessels with scrubbers, using low-sulfur fuel oil, or improving operational efficiency. Non-compliant vessels are being retired, further tightening the supply of available ships.

This regulatory push has led to a record order book for shipbuilding. In 2024, container ship newbuildings with a combined capacity of 4.4 million TEU were contracted, pushing the global order book for boxships to a record 8.3 million TEU.

Geopolitical Events Amplify Demand

The Red Sea crisis has further bolstered demand for vessels. Trade rerouting through the Cape of Good Hope has created a surge in shipping requirements, leading fleet owners to delay scrapping older vessels to meet immediate capacity needs. These dynamics, combined with rising regulatory costs, have maintained elevated ship prices even as raw material costs fall.

Steel vs. Shipping

The disconnect between HRC and ship prices highlights the unique dynamics of these interconnected markets. Steel, as a raw material, is subject to global oversupply, economic slowdowns, and intense pricing competition, particularly from Asian manufacturers. Conversely, ship prices are influenced by structural shortages, compliance with stringent environmental standards, and geopolitical events.

This paradox reflects the nuanced forces at play: while ships are predominantly made of steel, vessel prices are also driven by decarbonization mandates, supply shortages, and global trade dynamics.

The global HRC market is expected to remain under pressure in the short term. In the Persian Gulf and other regions, the dominance of low-priced Asian suppliers and muted demand from steel-consuming industries will likely sustain the current bearish sentiment. For exporters, managing excess inventory and finding competitive pricing strategies will be crucial.

In the shipping sector, the upward trajectory of vessel prices is unlikely to abate. The continued push for decarbonization, coupled with geopolitical disruptions, will sustain demand for modern and compliant ships. As shipping companies focus on fleet modernization and operational efficiency, shipbuilders stand to benefit from this wave of investment.

This divergence in trends underscores the complexities of global markets, where raw material prices, regulatory landscapes, and geopolitical events converge to shape outcomes. For stakeholders, adapting to these evolving dynamics will be essential for navigating the challenges and opportunities ahead.

Comments

No comment yet.