The Turkish Steel Producers Association (TÇÜD) has released production, consumption, and foreign trade data for July 2025. According to the figures, Türkiye maintained its position as Europe’s largest steel producer and the world’s seventh-largest, despite a 0.9% decline in cumulative production over the first seven months of the year.

Global crude steel production fell by 1.3% year-on-year in July 2025, totaling 150.1 million tons. In contrast, Türkiye’s crude steel output rose by 4.2% compared to the same month last year, reaching 3.2 million tons. During the first seven months of 2025, global production decreased by 1.9% to 1.1 billion tons, while Türkiye recorded a 0.9% decline to 21.5 million tons, retaining its top position in Europe.

Looking at finished products, flat steel production rose by 11.8% to 1.4 million tons in July, while consumption jumped 64.5% to 1.9 million tons. Over the seven-month period, flat steel production fell by 3.7% and consumption by 2.2%. For long products, production increased by 6.9% to 2.3 million tons in July, with consumption up 8.3% to 1.8 million tons. Year-to-date, long product production rose 7.3% and consumption 5.7%.

Overall finished product output rose 8.7% to 3.6 million tons in July, with consumption increasing 31.1% to 3.6 million tons. Over the first seven months, finished product production grew 2.8% and consumption 1.7%.

Exports declined in July

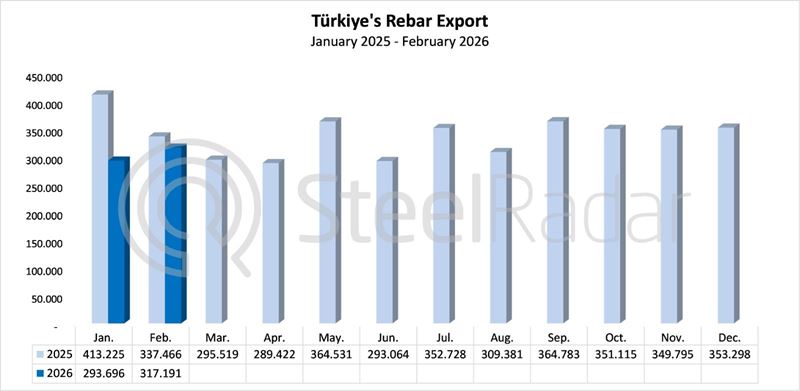

Türkiye’s steel exports fell 8.5% in volume terms compared to July of the previous year, although exports increased 13.9% over the first seven months of 2025.

Steel imports, however, surged 55.1% in July. Long products rose 26.6%, flat products 73.3%, and semi-finished products 43%. In the first seven months, imports increased 17.8%, with long products up 17%, semi-finished products 28.3%, and flat products 9.9%.

Scrap imports fell 6.1%

While crude steel production fell 0.9% in the first seven months of 2025, semi-finished product imports led to a 6.1% decline in scrap imports. The European Union accounted for the largest share of scrap imports, rising 1.9% compared to the same period in 2024. Scrap imports from CIS countries increased by 35.5%, while other regions saw decreases.

The export-to-import coverage ratio, which was 75.79% in the first seven months of 2024, declined to 76.99% due to the high import volume in July despite earlier increases in exports. Over the seven-month period, imports accounted for 48.5% of total steel consumption. In flat products, the import share reached 68.6%, with domestic inward processing (DİR) accounting for 58.4% of total imports, 74.1% in semi-finished products, 47.8% in flat products, and 38.6% in long products.

“The 55.1% increase in imports has caused serious concern in our steel sector.”

TÇÜD Secretary General Veysel Yayan stated: “The 55.1% increase in imports in July has caused serious concerns in our steel industry. Particularly, imports under the inward processing regime (DİR) from China, Russia, and other Far Eastern countries have intensified these concerns. In some products, DİR imports approaching 100% compete with domestic production, limiting the added value achievable through exports. This situation runs counter to the main purpose of DİR. Revising the DİR implementation is critical not only to restore the export-to-import ratio to 100% for our steel industry but also to prevent trade diversion from countries applying additional protection measures due to US and EU tariffs and to help balance the current account deficit.”

Comments

No comment yet.