Asia

In Asia, billet prices showed modest signs of improvement as producers tested the market with slightly higher offers. An Indonesian mill lifted its export offer by $3 per tonne to $438 FOB for January shipment. Chinese traders followed a similar path, raising their offers to $425–427 per tonne FOB for December shipment, compared with $423–425 a week earlier.

However, market participants say these small adjustments are more of a psychological test than an indication of real demand recovery. The region remains heavily supplied, particularly by Chinese exporters who continue to offer non-VAT wire rod at aggressive prices. This has put considerable downward pressure on billet values, not only in Southeast Asia but across the wider region.

According to international trading sources, 3SP billet was most recently offered at $427 per tonne FOB China and $438 per tonne FOB Indonesia. Yet, despite these small increases, buyers remain hesitant, preferring to observe how Chinese export volumes and domestic policies evolve before making large-scale purchases.

Türkiye

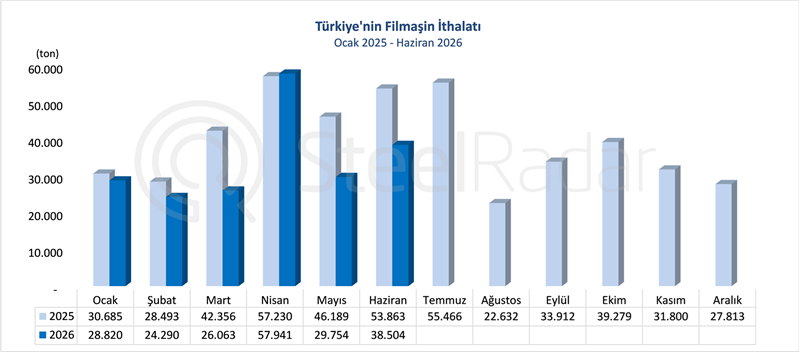

Türkiye continues to serve as one of the few consistently active destinations for large billet cargoes, though buyers are showing growing resistance to higher prices. Import activity has held steady, with prices hovering around $450 per tonne CFR, while domestic mills have maintained their offers at $500–502 per tonne FOB and $500 per tonne EXW.

Recent trade activity underscores Türkiye’s importance in absorbing Asian and Middle Eastern supply. Around 50,000 tonnes of Chinese billet were sold at $457 per tonne CFR Izmir for late November to early December shipment, while another 20,000 tonnes were booked to Iskenderun at similar levels. Malaysian suppliers also managed to conclude sales in the $485–490 per tonne CFR Türkiye range.

Most market participants agree that Türkiye’s import appetite is unlikely to expand unless Asian suppliers adjust prices downward. “Everyone is watching China,” said one Istanbul-based trader. “If they start flooding the market again, prices here will quickly follow.”

Middle East

In the Gulf region, sentiment remains largely steady, supported by a mix of stable domestic demand and selective export activity. Iranian billet suppliers continue to face foreign exchange-related hurdles but have managed to maintain pricing stability. Most major producers are offering $415–420 per tonne FOB for November–December shipments, while Esfahan Steel Co. (ESCO) reportedly sold 30,000 tonnes at $420 per tonne FOB through a tender.

Elsewhere in the region, buyers and sellers remain at odds over pricing. Both China and Indonesia have been offering billets to the UAE at $455–460 per tonne CFR, but buyers have been bidding closer to $450, resulting in no confirmed deals so far. Despite this, the price gap remains narrow enough to suggest that fresh transactions could emerge if freight costs or currency conditions shift slightly in favor of buyers.

Domestic producers in Saudi Arabia and Oman continue to enjoy relatively strong local demand. Prices in Saudi Arabia range between $480 and $507 per tonne EXW, while Omani offers remain firm at $485 per tonne FOB, showing little pressure to discount at this stage. Overall, the region’s billet market appears stable but cautious, with participants preferring short-term arrangements over long-term commitments.

Russia and CIS

Russia’s steel industry continues to struggle with weak domestic demand and declining output. According to Severstal, steel consumption in Russia fell to around 9.2 million tonnes in the third quarter, marking one of the lowest levels in recent years. The company’s data show a 15% year-on-year decline in overall steel demand during the first nine months of 2025, underscoring the depth of the downturn in local activity.

Severstal’s CEO Alexander Shevelev noted that crisis trends in both the Russian and global metallurgical sectors are deepening, with business activity slowing across all major consuming industries. Despite a sevenfold increase in pig iron and slab exports to 0.73 million tonnes, Severstal’s commercial steel sales declined by 8%, totaling 3.35 million tonnes.

On the export side, Russian billet activity has been subdued. Prices for early December shipment are currently quoted at $440–445 per tonne FOB Black Sea, slightly below earlier offers. Market sources say demand weakened in September due to falling prices and unstable offers from Chinese competitors at a time when buyers were contracting for autumn cargoes. Additional congestion at Black Sea ports, caused by seasonal cargo inflows, further delayed shipments and discouraged new deals.

Deliveries to nearby markets such as Georgia have continued at relatively stable levels, with Russian and Iranian billets being delivered at $440–450 per tonne CPT, roughly in line with the broader regional pricing trend.

Despite small upward movements from some Asian suppliers, the global billet market remains finely balanced between supply pressure and hesitant demand. Chinese exporters continue to dominate sentiment across regions, while the slowdown in Russia and seasonal factors in Europe and the CIS are limiting any potential recovery.

Market participants generally expect prices to stay within a narrow range through the remainder of the fourth quarter. Further gains appear unlikely without a clear improvement in end-user demand or a reduction in Chinese export volumes. For now, the market is characterized by selective buying, thin margins, and a cautious tone as traders prepare for a typically quiet winter season.

Comments

1 comments