In this interview with Laila Matta, Head of Scrap and Paolo Sangoi, Head of Steel at ASSOFERMET, which we met at the Made in Steel Fair, we discussed in detail the effects of the restrictions to be imposed on European scrap exports, the multi-dimensional effects ranging from competitiveness to carbon footprint, the current picture of Italy's steel production and the new opportunities emerging in the framework of competition with countries such as Türkiye.

Matta pointed out that scrap is a strategic resource in Europe's steel transformation, while Sangoi shared solutions to the pressure on production caused by the European Green Deal and the competitive imbalance caused by imports.

Laila Matta, President of Scrap at ASSOFERMET

What is ASSOFERMET's strategy for the future of scrap trading?

ASSOFERMET has always stated that the availability of recycled steel in Europe is significantly higher than demand.

The recycling industry recovers an average of 100 million tons of recycled steel in the EU each year, less than 20% of which is exported without a buyer. The export of these materials, which is in constant surplus due to the structural decline in EU steel production, represents a fundamental cornerstone of the Union's circular economy. The strategy of ASSOFERMET, in collaboration with EURIC (European Recycling Association), is to defend free trade in scrap, but above all to defend the European metal recycling industry, which plays a crucial role in the circularity and lower carbon footprint of the metal industry within and beyond the EU.

Therefore, instead of introducing new restrictions that could weaken the competitiveness of EU recyclers, ASSOFERMET calls for the removal of trade barriers between Member States, increased measures to promote the use of recycled materials in Europe, the introduction of recycled content requirements in industrial products, the adoption of Mandatory Green Public Procurement criteria that prioritize recycled materials, the financial support of research and innovation for the recycling sector, the reduction of bureaucracy and the digitalization of processes.

ASSOFERMET, as the voice of the Italian metal recycling industry, strongly warns against any additional restrictions on recycled metal exports beyond those already set out in the revised Waste Shipment Regulation, which has introduced new strict rules for EU recycled metals that will ensure that receiving countries comply with high environmental resource management standards.

Imposing additional export restrictions when there is no material shortage, when demand in Europe is at an all-time low and when there is no obligation to substitute raw materials with recycled ones would contribute to artificially lowering the price of recycled metals and ultimately destroying the European recycling industry. From a waste perspective, this would lead to a reduction in collection rates and an increase in landfilling as there would be no economic return from recycling high quality metals. From an industrial perspective, recycling facilities will be reduced or even shut down, leading to closures and job losses.

The recycling industry is the backbone of the decarbonization process of the European steel industry

What approaches do you envision to overcome potential restrictions and barriers to scrap exports? How would this affect the sustainability of the sector?

The European Steel and Metals Action Plans are considering reciprocalizing export restrictions and potentially introducing “export fees or taxes on recycled metals”. Such measures risk creating new trade barriers that could harm the functioning of global recycling markets and, in particular, European metal recyclers.

Moreover, obstructing recycling through protectionist measures would mean backtracking and slowing down the achievement of the environmental and decarbonization targets set by the EU.

As extensively discussed, and underlined in previous questions, we need economic incentives for research and development, targeted interventions to reduce energy costs, mandatory recycled content targets for metal products, mandatory inclusion of a minimum percentage – let’s say 30% - of recycled materials in public procurement.

Without taking the concrete steps mentioned above, simply “banning the export of recycled steel” will not solve the problems of the European steel industry, it will not boost the European steel industry, it will only harm the European recycling industries.

The recycling industry is the backbone of the decarbonization process of the European steel industry, therefore we ask the European Commission to recognize its fundamental role and to support it financially to sustain it and put it in a position to provide a new source of increasingly high quality - recycled steel.

.jpeg)

Paolo Sangoi, President of Steel at ASSOFERMET

“US trade barriers could have a domino effect for Italy and the entire European Union”

How do you evaluate the current status of Italy's steel production and exports? What opportunities and challenges do you face in competing with countries like Türkiye?

In 2024, total steel production in Italy decreased by 5% compared to 2023. The decline was even more pronounced in the flat products segment, amounting to around 10%. The main reasons for this contraction are the crisis that hit ADI (excluding ILVA) and the general decline in both national and international consumption.

The figures for the first quarter of 2025 show signs of recovery. Total production increased by 3.1%, while long products decreased by 0.9% and flat products increased by 9.1%. However, given the uncertainty in the global macroeconomic context, these figures should be interpreted with caution.

Exports is a significant component of the Italian steel sector. In 2024, in value terms, exports contracted by 10% compared to the previous year. Germany remains the main destination market, but the German consumer crisis has inevitably affected the export volume.

Concerns are also growing about the impact of the US protectionist policy. Although Italian exports to the US are mainly related to high-performance steel, which is not readily available on the US domestic market and is therefore partly protected, any new restrictions could still have negative repercussions.

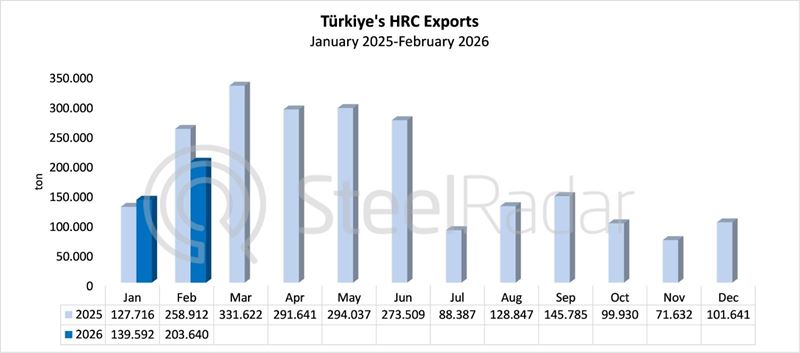

Another focus of interest is Türkiye, the world's eighth largest steel producer, which exported more than 13 million tons in 2024. The flow of Turkish steel to Italy is constant and strategic for many buyers thanks to geographical proximity and the wide dimensional range offered. However, Türkiye's growing production capacity, together with some Far Eastern countries, raises concerns. In particular, the tightening of trade barriers by the US could create a domino effect with destabilizing consequences for Italy and the entire European Union.

What are the main challenges facing industry at this time? In what ways are ASSOFERMET members working to develop effective solutions to address these challenges?

The sector represented by ASSOFERMET Acciai, which includes the first transformation and distribution of steel, is a reality of excellence in the Italian industrial panorama, with more than 13,000 employees and a turnover of more than 20 billion euros. This sector ensures a continuous supply flow to the main steel users, including automotive, household appliances, construction and many other strategic production sectors.

Thanks to know-how consolidated by decades of experience, the sector can rely on the supply of high-quality steel from leading European and international steel mills. Thus, it has significantly contributed to the development of European manufacturing, strengthening the competitiveness of the whole industry.

However, recent protectionist policies and particularly stringent environmental regulations jeopardize a significant portion of the current supply sources. This scenario risks compromising the ability to ensure stable and quality supply to end users.

In this context, ASSOFERMET is constantly in an active dialog with the Italian and European institutions in order to accurately and constructively represent the complexity of the steel sector so that the choice of legislation takes into account the real operational and economic needs of the supply chain.

How do the European Union's policies and regulations, particularly concerning environmental standards and carbon emission targets, impact steelmakers in Italy? How does competition evolve between the EU and other countries in this regard?

The European Green Deal, although an ambitious and environmentally far-sighted project, has proven to be insufficiently adapted to economic and productive reality. The accelerated implementation, especially with tight deadlines, has already had tangible negative effects and strategic sectors such as the automotive industry risk an unprecedented crisis, if not a complete disintegration of its industrial model.

The drop in demand from automotive manufacturers has a direct and severe impact on the production of steel mills, which are already suffering from a structural and sustained market contraction. Added to this scenario is the further aggravation of production costs linked to the ecological transition that European steel mills will have to face through the conversion of a large number of plants to electric steelmaking in order to comply with the objectives of the Green Deal.

Further complicating the picture is the lack of an effective strategy to extend environmental regulations also to finished products imported from non-EU countries. These products, often produced under less stringent environmental conditions, are not subject to any carbon tax or compensation for their ecological footprint, thus creating an unfair competitive situation to the detriment of European production.

Can provide an evaluation of Italy's approach to steel imports? What are your views on the current production in Italy as well as the consequences of EU countries looking for alternative imports?

I do not blame domestic producers, who are facing a worrying drop in demand and an increase in production costs, also linked to the dynamics described above, but I contest the idea that these challenges can be solved simply by raising new trade barriers.

This strategy, in fact, risks triggering a significant increase in steel prices within the European Union, while ignoring the serious repercussions on the entire European manufacturing industry. An increase in the cost of raw materials compromises the international competitiveness of our companies, which are already severely tested, and ends up fuelling a process of deindustrialisation that appears increasingly difficult to stem.

Comments

No comment yet.