On the second day of the BIR's World Recycling Convention, which took place in Amsterdam between 22-24 May 2023, the experts of the recycling world continued to convey their research and observations. "The effects of the energy crisis, which started with Russia's occupation of Ukraine, on the global market and on Europe" was one of the main topics.

While President of BIR Ferrous Division Denis Reuter announced the release of the 14th edition of "World Steel Recycling in Numbers" covering the five-year period from 2018 to 2022, BIR's Statistics Advisor Rolf Willeke shared some of his key findings with the audience.

Referring to the BIR Ferrous Metals Board's decision to replace the term steel scrap with recycled steel, Willeke stated that they aim to resonate more effectively publicly and politically. “The term also reinforces the importance of recycled steel for green steel production.” He underlined that we have entered a new era of communication.

Referring to worldsteel data on global steel production, the speaker said, “Global crude steel production amounted to 1885.0 million tons last year, a decrease of 3.9% compared to 2021. The data show a decline in crude steel production in all regions of the world except the Middle East.' According to the information obtained from the SteelRadar reporter, it was emphasized that although production decreased by 1.8 percent to 1384.8 million tons, Asia remained the world's largest crude steel producer. China remained the world's largest user of recycled steel, although it fell 4.8 percent to 215.31 million metric tons. Turkey, one of the most important buyers of recycled steel, is also of great importance in this context. Despite a 16.5 percent decline to 20,876 million metric tons in recycled steel imports, Turkey did not lose the top spot. Turkey, furthermore, imports recycled steel mostly from the USA, the Netherlands and the UK, respectively.

Later, Ole Rolser, the team leader of Global Energy Perspective at McKinsey & Company gave his influential presentation, and detailed the main idea and theme of his speech under the title of "European and global energy in the new era post Russia's invasion of Ukraine".

Rolser said, "Europe's energy expenditure on oil, gas and coal rose from 4% to 10% of GDP last year and will remain high through 2025. For any future prediction we need to look at scenarios regarding the pace of technological advances and the level of political implementation. Energy demand outlook continues to see a slowdown as a result of energy efficiency and electrification."

War in Ukraine causes record high global gas prices in 2022

Rolser added, “2021 witnessed strong growth in LNG demand due to the post-Covid-19 recovery, with limited additions to LNG supply. The outbreak of war in Ukraine and the subsequent decrease in Russian piped flows triggered gas supply restrictions in Europe and the need to import extra LNG as a backup. The limited availability of LNG has led to increased competition for spot cargo, which has led to record high prices at global gas centers.'

Rolser also listed some developments in articles;

- While global prices return to pre-war levels, they remain about 50% above historical levels, indicating a structural shift in the market.

- Historically, Europe has relied on Russian gas to meet 32% of the supply. Germany, Italy and Poland were the most exposed countries.

- Europe stabilized the gas market by reducing gas consumption in buildings and industry by 11%;

- Industrial efficiency gains and behavioral change in heating for buildings have been the main drivers of demand reduction.

All these developments 'Energy-intensive industrial sectors, while causing significant production cuts in 2022, started to recover in the 4th quarter.' Ole Rolser told the following about the developments of the companies;

- US Steel Kosice stopped its second blast furnace in December.

- ArcelorMittal announced that it would close one of its two 2 million mt/year blast furnaces in Fos-sur-Mer in November.

- Duralex announced in November that it was shutting down its furnace for five months.

- Glencore stopped production in November at its 160,000-tonne zinc smelter in Nordenham, Germany.

- Nyrstar announced in December that it would not resume zinc production after scheduled maintenance.

- Trimet, St. Jean de Maurienne announced that it would reduce the capacity of its foundry by 20%.

- Kammerer Group shut down one of three specialty paper machines.

Rolser said the following about his future expectations;

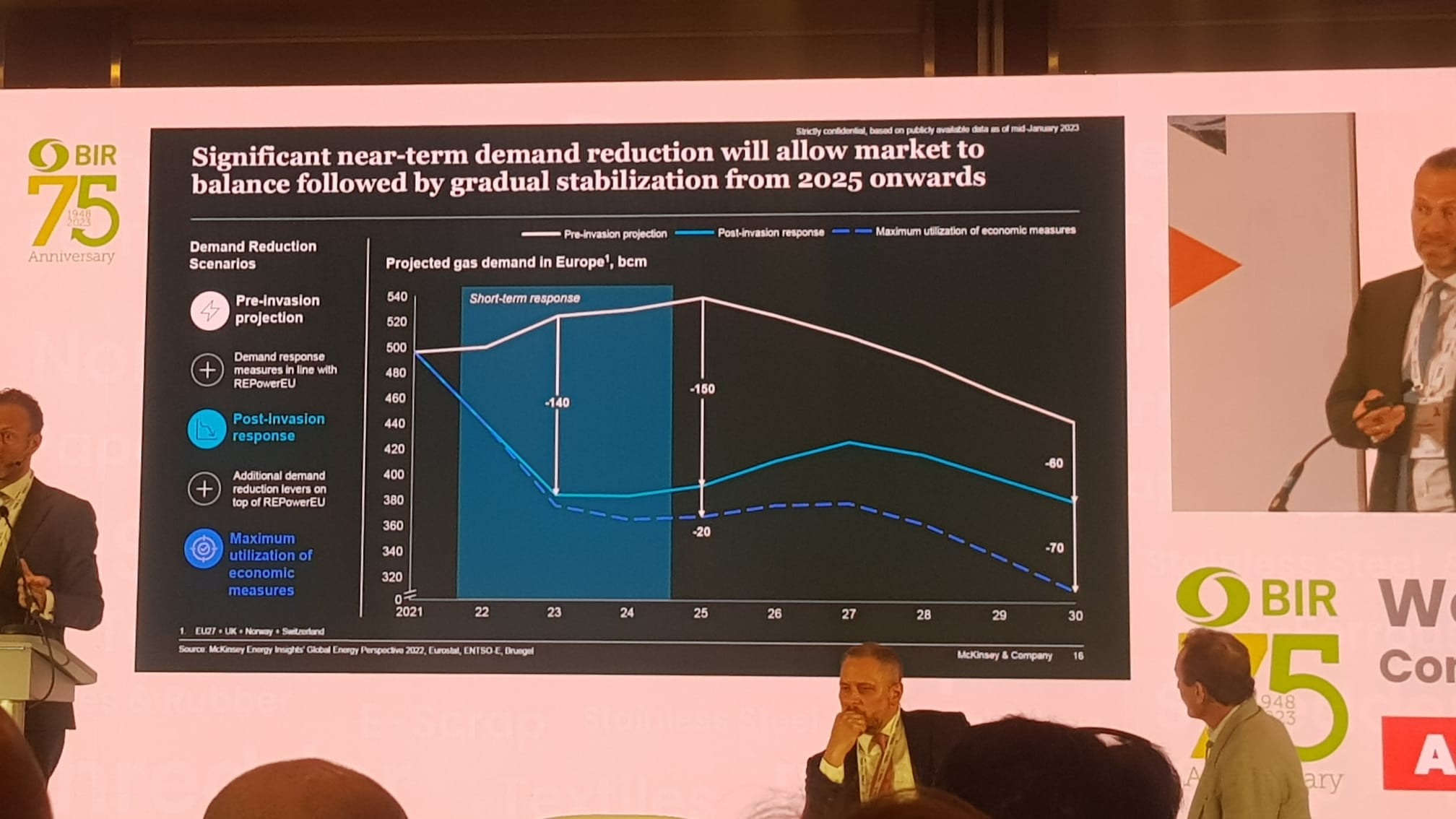

“Near-term demand decline will allow the market to stabilize, followed by gradual stabilization from 2025.

“Global LNG markets will remain critical into the mid-2020s, even after accounting for capacity under construction and pre-FID.”

Afterwards, Rolser added “Prices may be rebalanced to $9-10/mmbtu from 2026, while uncertainty continues” and listed what we should believe as follows;

- LNG supply chain disruptions + no Russian flow (eg <100 mtpa additional LNG capacity by 2030)

- Flexible gas demand in Europe and Asia (e.g. +35 bcm LNG demand from China)

- Price determined by gas-coal switching price 2021)

- New LNG developed in fast track mode (eg > 120 mtpa additional capacity by 2030)

- Flexible gas demand in Europe and Asia (eg +20 bcm LNG demand from China)

- Balanced markets, the price determined by the long-run marginal cost of liquefaction.

- -5-10% (-20-40 bcm) of EU demand is reestablished by Russian supply.

- Permanent gas demand destruction due to high prices and fuel switching.

- Abundant supply and price of security (eg '19-'20) determined by short-run marginal cost of liquefaction.

- Increased durability for industrial players should include optimizing their own and grid power.

Comments

No comment yet.