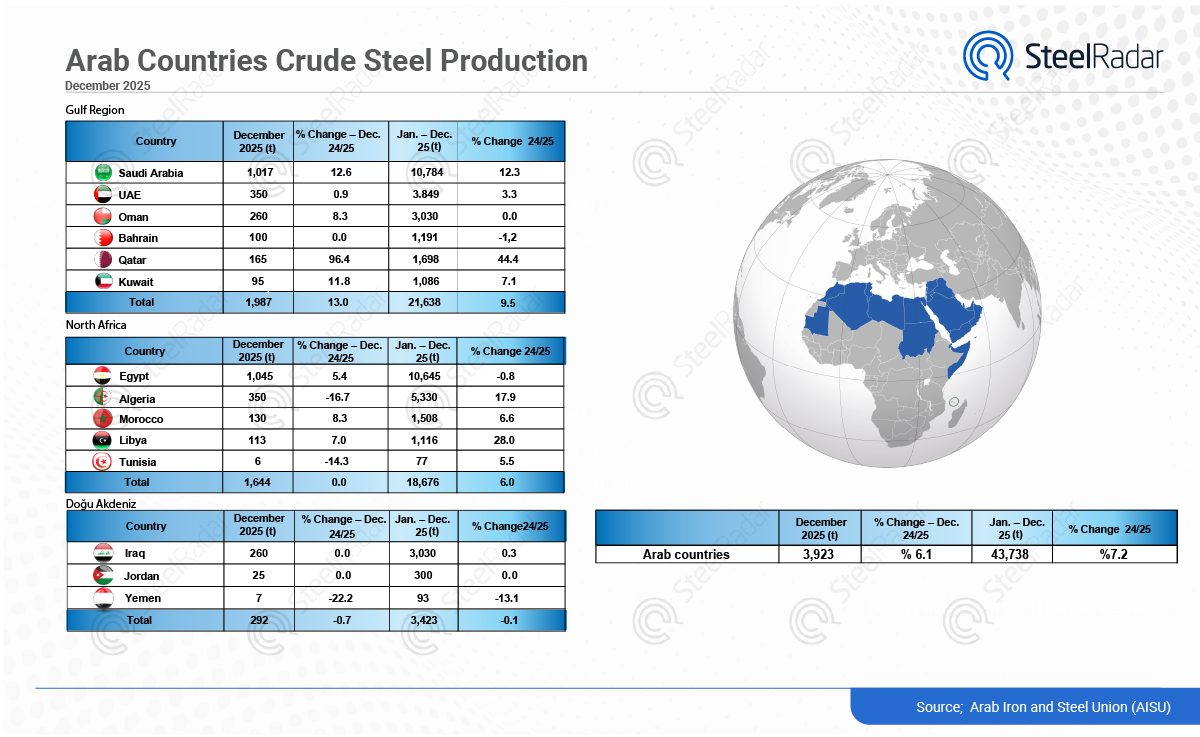

According to World Steel Association data, the region's total crude steel production increased by 7.2% during the January–December 2025 period, reaching 43.738 million tons. December output stood at 3.923 million tons, marking a year-on-year increase of 6.1%.

Production growth stood out in the Gulf

Among Gulf countries which account for the largest share of regional output total production rose 9.5% to 21.638 million tons. December production surged 13% to 1.987 million tons.

Saudi Arabia maintained its leadership position with output rising 12.3% to 10.784 million tons. The UAE recorded a 3.3% increase to 3.849 million tons, while Qatar posted a robust 44.4% growth, reaching 1.698 million tons. Oman remained flat at 3.030 million tons, Bahrain declined 1.2% to 1.191 million tons, and Kuwait rose 7.1% to 1.086 million tons.

Demand pressure persisted in the long products segment across the region, while flat products and scrap markets displayed a more balanced outlook. Demand for high quality scrap remained particularly strong in the UAE.

Gradual growth in North Africa

North Africa's total production increased 6% to 18.676 million tons. Egypt's output edged down 0.8% to 10.645 million tons, while Algeria surged 17.9% to 5.330 million tons. Libya rose 28% to 1.116 million tons, Morocco increased 6.6% to 1.508 million tons, and Tunisia remained at 77,000 tons.

In semi-finished and construction steel trade across the African region, suppliers have adopted more flexible strategies, while buyers continue to be influenced primarily by logistics costs, financing conditions, and demand expectations.

Stable outlook in the Eastern Mediterranean

Production in the Eastern Mediterranean region totaled 3.423 million tons, dipping slightly by 0.1%. Iraq's output rose 0.3% to 3.030 million tons, Jordan remained flat at 300,000 tons, and Yemen declined 13.1% to 93,000 tons.

Overall, 2025 emerged as a year of continued production growth across the region, with evolving demand patterns shaping trade dynamics and product strategies. Strong expansion in the Gulf, steady gains in North Africa, and stability in the Eastern Mediterranean all point to the ongoing progression of regional capacity additions.

Comments

No comment yet.