In the United States, winter storms stretching as far as Texas intermittently shut down recycling facilities, disrupting the supply of obsolete-grade scrap in particular. According to the World Mirror publication of the Bureau of International Recycling (BIR) Ferrous Division, the diversion of significant volumes of recycled steel into the export channel also paved the way for price increases in the domestic market.

In Japan, a more stable trend has been observed in the recycled steel market in recent months, supported by a slowdown in production and the continued depreciation of the local currency. In China, crude steel production declined by 4.4% last year to approximately 961 million tonnes, while exports reached a record 119 million tonnes. Despite ongoing efforts to implement capacity reforms, Chinese steel is expected to remain a source of pressure in global markets.

In India, the increase in steel demand in 2025 was driven by the construction, infrastructure, and automotive sectors. Domestic mills preferred locally produced direct reduced iron (DRI) over imported recycled steel due to its lower cost and easier availability. Deep-sea scrap importers, meanwhile, faced regional competition from Bangladesh and Türkiye.

In Europe, the German recycled metal sector is expected to face shortages amid weak industrial and construction volumes and irregular demand from electric arc furnace mills. Shrinking profit margins may trigger further consolidation within the sector, while harsh weather conditions have negatively affected recyclers’ operating levels in Scandinavia.

In the United Kingdom, prices have risen recently, with intense competition for shredding feedstock. Significant market volatility has been observed, and the bankruptcy of Unimetals, along with the closure of several companies including long-established firms, has highlighted the challenges facing the sector.

In the Middle East, recycled metal prices increased in the United Arab Emirates due to strong buying interest and export demand, while the market in Saudi Arabia remained relatively flat, with buyers focusing on selective restocking.

In South Africa, the government’s failure to clarify the long-term structure of the Price Preference System (PPS) and the export tax regime has created uncertainty, weighing on trading activity and weakening confidence across the steel value chain. PPS and export restrictions are said to have kept recycled steel prices in the country below global market levels.

According to the “World Steel Recycling Figures” update published by BIR Ferrous Division Statistics Advisor Rolf Willeke, recycled metal consumption declined y-o-y in China, the EU-27, the United States, Japan, and South Korea during the January–September period of last year. In contrast, consumption in India increased by 16% to 29 million tonnes, outpacing the 10.5% rise in crude steel production (122.4 million tonnes). In Turkey, crude steel production rose by 0.7% to 28.1 million tonnes, while recycled steel usage increased by 4.3% to 24.456 million tonnes.

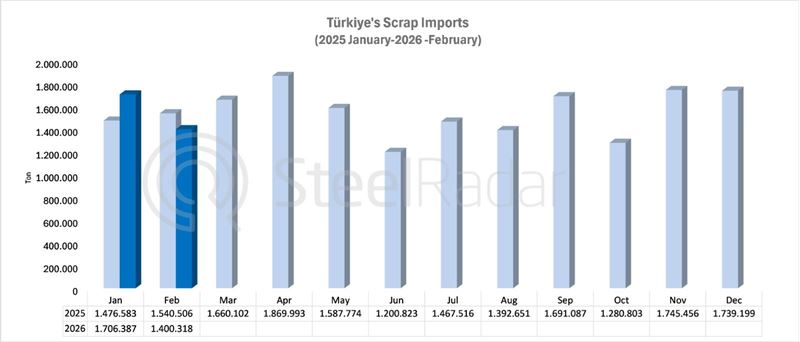

On the trade front, Türkiye remained the world’s largest importer of recycled steel despite a 6.8% decline in imports to 13.988 million tonnes in the first nine months of 2025. India strengthened its position as the second-largest importer, with volumes rising 2.8% to 6.54 million tonnes. Meanwhile, the EU-27 maintained its status as the world’s largest exporter of recycled steel, even though exports fell by 4% to 11.939 million tonnes during the same period.

Comments

No comment yet.