Despite a limited improvement in finished product production, the report notes that almost the entire increase stemmed from the restart of operations at the Nová Huť plant in Ostrava. The sector's weak outlook is driven by low demand, high energy costs, pressure from low-priced imports from third countries, global geopolitical developments, high and volatile prices for emission allowances, and additional costs arising from the European Green Deal.

Long-term decline in production continues

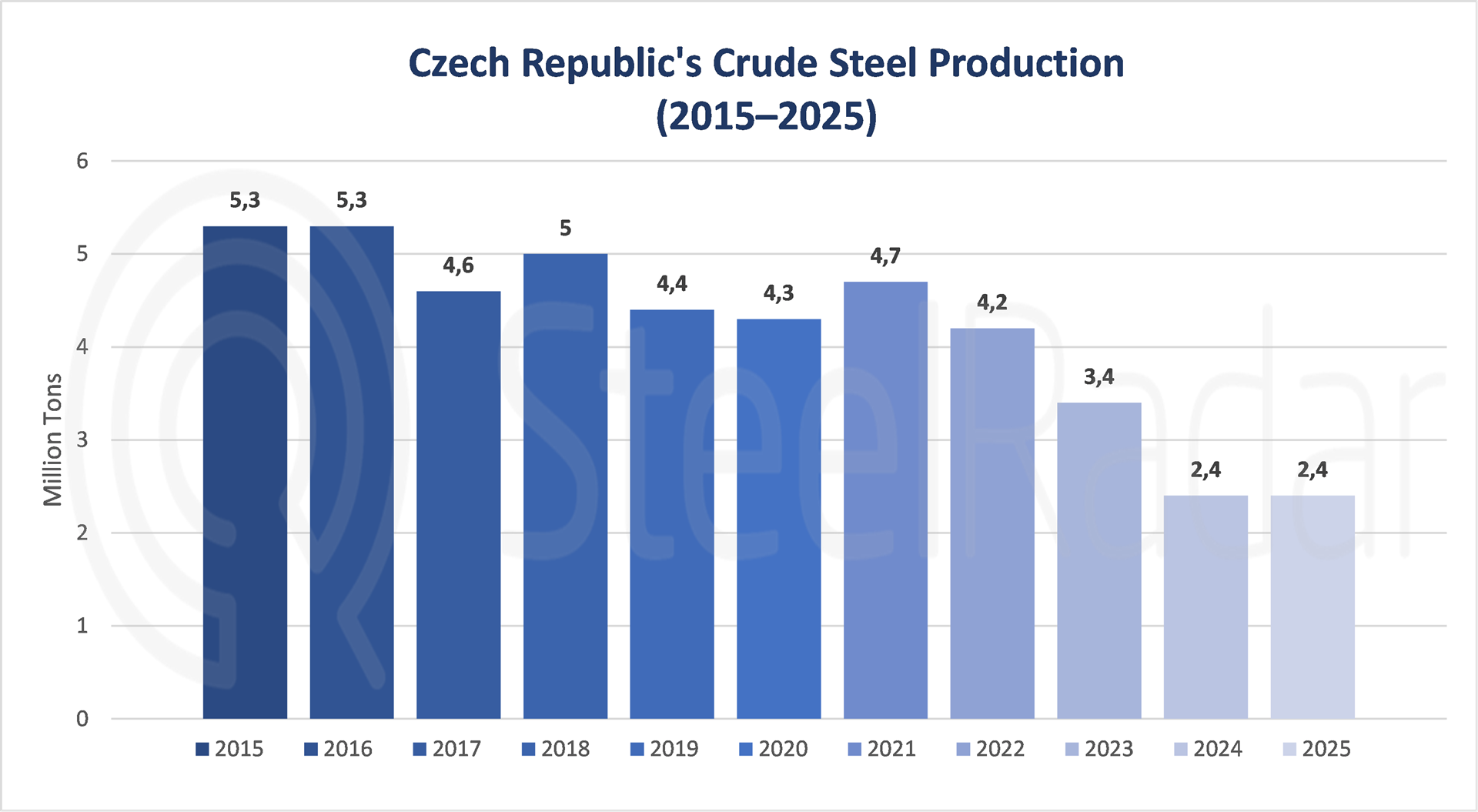

The Czech steel industry has experienced a significant long-term decline. Unlike the former Czechoslovakia, which ranked among the world's leading steel producers with per capita production of around 1 ton until the early 1990s, today's output has fallen sharply. In 2025, the country produced 2.4 million tons of crude steel, virtually unchanged from the previous year and marking one of the lowest levels in history. Over the past decade, production has dropped by more than 50%, with the 2015 figure of 5.3 million tons declining particularly due to the termination of primary production by the Ostrava-based Liberty company (now known as Nová Huť).

Weak consumption, limited recovery in finished products

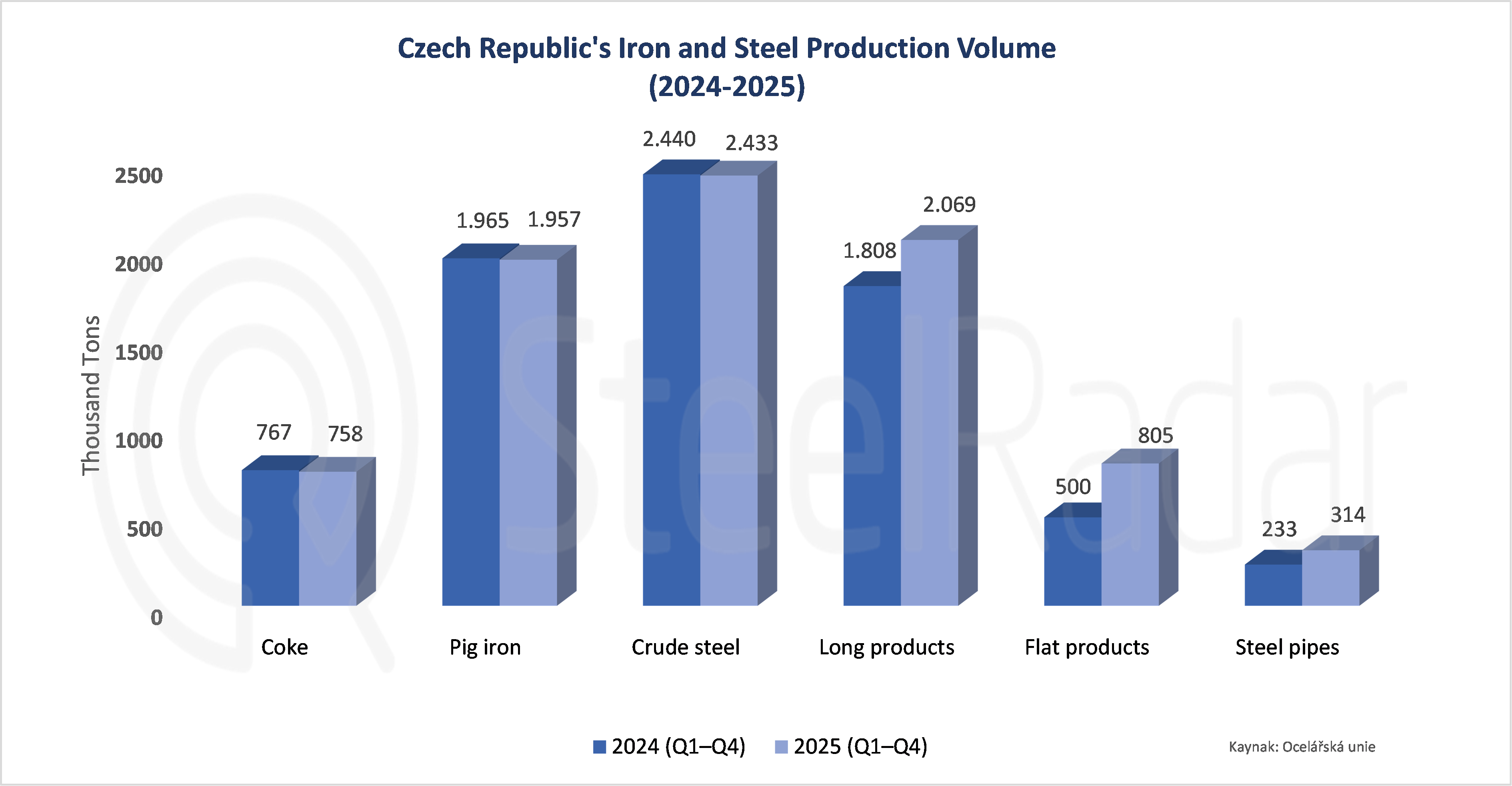

On the consumption side, a modest recovery was observed. Apparent steel consumption in 2025 rose to 5.5 million tons, though this level ranks as the second-weakest performance since the 2009 global financial crisis. While finished product production saw a year-on-year increase, the rise in long and flat products was largely attributed to the resumption of production at the Nová Huť facility. Overall finished product output remained at 2023 levels. In 2025, long product production exceeded 2 million tons, flat product production reached 805,000 tons, and steel pipe production increased to 314,000 tons.

Cost and import pressures persist on the sector

Roman Heide, Chairman of the Supervisory Board of the Czech Steel Union and CEO of Třinecké železárny, highlighted the challenges facing the industry, stating that external factors weakening economic stability across Europe have deeply impacted the steel sector. Heide emphasized that low-priced imports from third countries, high energy costs, and volatility in emission allowance prices are severely undermining the competitiveness of European producers. He also pointed to the unpredictable nature of the emissions trading system, noting that costs are continuously rising and further eroding competitive strength. Given the current geopolitical conditions, he added that the sector's outlook remains highly uncertain.

Growing foreign trade deficit

The decline in production has negatively affected the foreign trade balance as well. While the Czech Republic's steel trade balance deteriorated markedly in recent years, the deficit, which stood at around 1.6 million tons about a decade ago, has now exceeded 4 million tons. In 2025, steel product imports rose by 900,000 tons year-on-year to 7.5 million tons, with a total value of 172 billion Czech koruna. During the same period, exports showed more limited growth, reaching 3.4 million tons with a total value of 96 billion koruna.

Global production declines, strong growth in India

On a global scale, steel production contracted. In 2025, world crude steel output fell by 2% to 1.803 billion tons (according to World Steel Association data; note: some sources report the final annual figure at approximately 1.849 billion tons with slight variations in estimates). China, despite a 4% decline, maintained its leadership with 961 million tons, accounting for roughly 53% of global production. In contrast, India recorded robust growth as the world's second-largest producer, exceeding 10% increase to reach 165 million tons and nearly doubling its output over the past decade. Production increases were also notable in emerging economies such as Vietnam, Saudi Arabia, and Algeria.

EU production continues downward trend Across the European Union, production maintained its declining trajectory. In 2025, total EU steel output decreased by 2.6% to 126.2 million tons. Germany, despite an 8.6% drop, remained the bloc's largest steel producer but experienced one of the steepest declines among leading countries.

Comments

No comment yet.