While the rises were limited, the fact that most products remained in positive territory indicated that the market is entering a recovery phase from the bottom. However, a strong momentum on the demand side still has not developed.

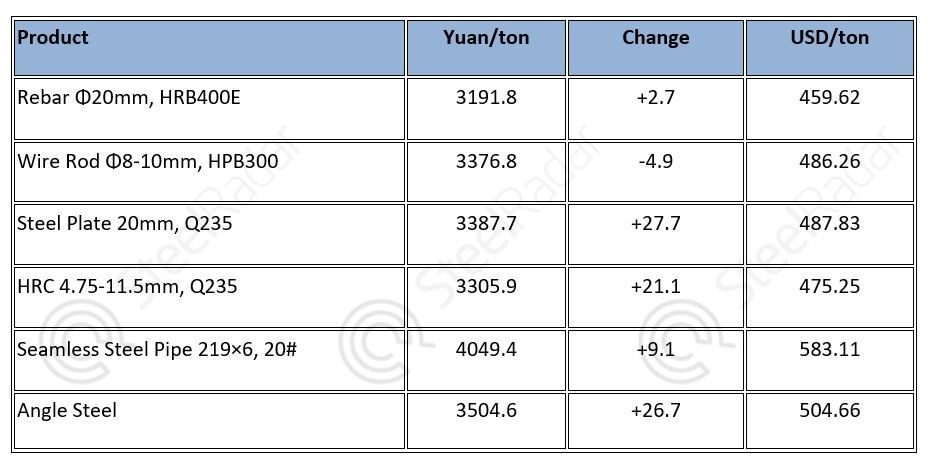

Price movements in flat products and structural steel segments showed a more noticeable upward trend. Medium-thick plate reached USD 488/ton, angle steel USD 505/ton, and hot-rolled coil USD 475/ton, increasing by 0.6–0.8%, reflecting relatively active industrial and manufacturing demand. In contrast, the limited rise in rebar at around USD 460/ton and the slight decrease in wire rod show that demand remains cautious. Seamless pipe prices stayed at approximately USD 580/ton, indicating that demand continues in some industrial sectors.

The China steel market shows limited recovery signals due to price increases and inventory reduction policies. Prices of specialized production inputs slightly increased, the manufacturing sector continues to grow, and new orders are rising, while inventories are decreasing. Rising energy costs, combined with global geopolitical tensions and supply disruptions caused by war, are putting pressure on costs.

The Beijing administration is trying to control the market through gradual reduction of steel production capacity and inventory depletion policies. Green transition initiatives support the goal of reducing emissions in production. While excess supply pressure continues in the global steel market, protectionist measures remain on the agenda. Nevertheless, demand growth in countries such as India and China has generated limited recovery signals in the market.

Comments

No comment yet.